Negative interest rates have

been creating a buzz over the past few months. Paying interest for deposits,

instead of earning interest, is coming into vogue. The world of central banking

and economics is becoming more confounding by the day.

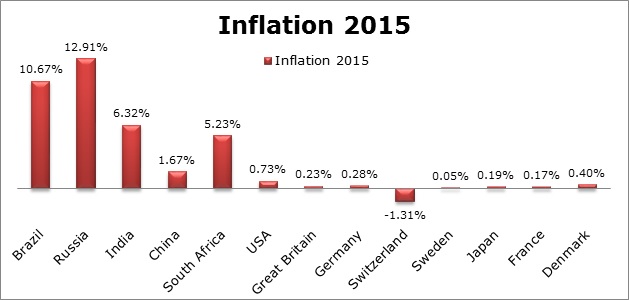

An overview of the inflation

across some of the major economies of the world in 2015 is as below. Near zero

inflation is one of the key driving factors behind the Negative Interest Rates.

The emerging economies are

struggling with a high inflation rate. Prices are on the rise across the BRICS

countries, causing a lot of pain among consumers. High inflation, as seen in

Brazil and Russia, is considered to have a negative impact on the economy.

|

| Inflation in 2015 |

On the other hand, the

advanced markets are dealing with a near zero or subzero inflation rate. In

2015, most of the economic powerhouses in Europe and the USA have recorded an

inflation rate less the

healthy benchmark of 2%. This

has the Central Banks across the advanced economies worried.

Meanwhile, the US Fed

increased the base rates for the first time in a decade in December 2015. The

oil prices are below 40 US Dollars a barrel. The slender inflation, and even

deflation in some countries, is impacting consumer growth in the advanced

economies. This in turn is impacting exporting countries like China. China is

in a slowdown.

In such challenging and evolving

economic conditions, central banks across the world are increasing adopting a

Negative Interest Rate Policy to manage the economy.

The

Actions by the Central Banks

It will be worthwhile to

understand the actions related to negative interest rates by different central

banks across the world.

The Danish National Bank

(DNB) was the first central bank in the world to adopt the Negative Interest Rate Policy in July 2012. The DNB has

currently set the deposit rate at minus 0.65% (-0.65%) as on 11th

March 2016. The certificates of deposit (typically a 7 day deposit) sold by the

DNB will attract a rate of -0.65%. With this, a bank placing a

Certificate of Deposit with the DNB will need to pay interest at 0.65%.

The next one to adopt this

policy was the European Central Bank (the ECB). The Deposit Facility Rate was

0% between May 2013 and Jun 2014, while it has been in the subzero territory

since Jun 2014. On 10th March 2016, the ECB reduced the Deposit

Facility Rate to minus 0.4% (-0.4%), as against the earlier rate of -0.3%. This

rate will be applicable when the banks make overnight deposits within the

Eurosystem.

Thus, commercial banks

placing a deposit with the ECB would need to pay interest

at 0.4%, rather than earn interest for the deposit.

The Central Bank of Sweden

(The Riksbank) is also using this policy. It has set the overnight deposit rate

at -1.25% since February 2016. The deposit rate is in the negative territory

since September 2014.

The Bank of Japan (BOJ) and

the Swiss National Bank (SNB) have also reduced the deposit rates below 0%. In

late January 2016, the BOJ set the benchmark rate at -0.1%. The SNB has set the

deposit interest rate at -0.75%, a historical low. With this measure, banks

need to pay interest for the deposits placed with the central bank.

It can be seen that negative

interest rates are being increasingly used as a central bank policy tool in

major economies across the world.

Why

Negative Interest Rates?

It will be critical to

understand the key reasons behind the negative interest rate policies.

Improving

Credit Growth

Many central banks (though

not all) across the world implement a Minimum Reserve Requirement. It is the

minimum portion of the customer’s deposits which the banks must maintain as

deposits with the central bank.

The Central Bank pays

interest to the commercial banks for the deposits placed with it. This rate is

often referred to as the Deposit Facility Rate or the Reverse Repo Rate.

The Central Bank of the

country can also extend loans to the commercial banks in case of any shortfalls

or liquidity crunch. This rate is referred to as the Repo Rate or the Lending

Rate.

These rates are extremely

powerful tools for managing an economy. The rates directly control the

liquidity in the financial system, and the rates at which the bank will lend to

its borrowers.

Usually, the interest rate

offered by the Central Banks for overnight deposits or 7 day deposits is much

lower than the interest rate at which banks lend to consumers and businesses.

To maximize the profits, the banks tend to keep the deposits with the Central

Bank close to the required minimum and utilize the excess for lending.

However, in the throes of

difficult economic conditions, banks usually take a risk-averse position. The

opportunities for lending reduce in light of the stagnating economic weather,

due to reduced business opportunities or due to an unfavorable assessment about

the quality of the credit.

In such circumstances, instead

of lending to consumers and businesses, the banks prefer to park their excess

funds with the Central Bank. The funds available for lending are thereby

reduced. This leads to increased cost of borrowings, a credit crunch and may

lead to a downturn in the economy.

Central Banks are using

Negative Interest Rates to resolve this deadlock.

The move by the ECB and other

Central Banks is expected to encourage banks to lend money to borrowers to earn

interest rather than placing those funds in the safe havens of the Central Bank.

The negative interest rate policy is being used as a tool to prompt banks to

lend to businesses and corporations. The idea is to make the funds available to

enterprises needing them. The Central Bank is expecting to kick start the

economy and trigger a cycle of spending.

The SNB has implemented an

interesting variant of this policy. The SNB has a minimum reserve requirement.

The banks placing funds with the SNB in excess of 20 times of the minimum

reserve requirement (referred to as the exemption threshold) need to pay

interest at the rate of -0.75%. In short, central banks are implementing a tiered

model of deposit interest rates to penalize commercial banks for placing

additional deposits with the central bank.

In effect, to improve credit

growth and increase the inflation rate near the stable levels, negative

interest rates are being adopted by central banks.

Improving

Consumption and Investments

The commercial banks

continue to be cautious with respect to lending to businesses, in spite of

these nudges by the central bank. They continue to keep their excess funds with

the central bank. However, since the bank needs to pay interest rather than

earn interest on such deposits, the bottom-line of the banks are getting

impacted.

Banks are devising ways and

means to cushion against such reductions in profit. One of the techniques is to

the charge customers who save their money or place a deposit with the bank. The

customers would be expected to pay interest for their savings and deposits.

Paying for their own savings

is not an attractive option for the customers! This is worrying the banks too,

since customers may withdraw funds from the bank. However, the central banks

are keen to see this happening. They want to the consumers to spend instead of save, and once

again, kick start the economic cycle. Increase in consumption is expected to

help the inflation rise to the required levels.

In addition, due to lower

interest rates, it would be easier for corporations to finance their business

operations. This would lead to an increase in investments from such

organizations, which in turn is expected to trigger an increase in the demand

across the economy and a higher inflation.

Some banks are trying to

avoid a direct impact to the customers. Such banks are increasing the rate of

interest for loans and mortgages. This is increasing the cost of borrowing in

the market, much to the disappointment of the central banks. After all, the

central banks wanted the loans to be easily available for businesses, at

affordable costs of borrowing.

Another interesting theme

which is coming to fore recently is the concept of paying interest to the borrower for borrowing money. Yes,

you read it right – interest will be paid to the borrower, instead of the usual

norm of the interest being paid by the borrower.

Promoting credit growth is

one of the key aspirations of the central banks in the advanced economies

struggling with stunted inflation. Under a new scheme being evaluated by the

European Central Bank, the ECB could pay banks to borrow money from it, if they

extend significant loans to consumers.

This is related to the four

year loans being granted by the ECB under the new targeted longer-term

refinancing operations (TLTRO II) scheme. With this, the banks can get

refinancing from the ECB at 0% (the main refinancing rate was set at 0% on 16th

March 2016). The banks can also earn interest at rates up to 0.4% (the Deposit

Facility Rate is set at -0.4%) for refinancing from the ECB.

To sum up, using the tool of

negative interest rates, the central banks are expecting to increase

consumption, improve spending, increase investments and trigger a cycle of

growth.

Moderating

the Currency Exchange Rate

The world is experiencing

tough economic conditions. The markets are in turmoil. The price of oil is

hovering below 40 USD a barrel, down from 80 to 100 USD price range prevalent

in the last 5 years. The last time the oil was below 40 USD a barrel was in Nov

2003. The world has changed significantly in the last decade.

In such challenging circumstances,

stable markets like Switzerland see a sizeable inflow of funds. The continued

buying of the currency increases the value of the currency vis-à-vis the US

Dollars and other major currencies. This in turn leads to increase in imports,

reduction of exports, making the exports costlier and the economy less

competitive.

One of the intentions of the

SNB for reduction of the deposit rate below 0% is to discourage investors from

buying the Swiss Franc, avoid the over valuation of the Franc, and thereby keep

the Swiss economy competitive.

Nevertheless, customers continue

to keep deposits with the banks, even though the rate of interest is below

zero. As an illustration, foreign investors would be happy to place deposits

with banks in economically strong countries like Switzerland and Germany even

though the deposit rate is less than 0%. Such investors expect the exchange

rate of the Swiss Franc against other currencies to rise favorably, thereby favorably

offsetting the negative yield on the deposit.

The Swiss Government

recently borrowed money from the market at a rate of interest of -0.26%.

Needless to say, the investors did not shy away from such bonds. After all, the

Swiss Government bonds are considered to be absolutely safe, and the

probability of the Swiss Government defaulting is negligible, if not zero. Add to

it, the currency valuation of the Swiss Franc vis-à-vis the other major

currencies is expected to rise. All these positives make such bonds attractive.

In spite of a slew of

measures related to negative interest rates, the Swiss Franc continues to be

strong, causing worry in the SNB. To address this situation, the SNB is also

contemplating the reduction of the exemption threshold. The reduction of the exemption

threshold will make it increasingly difficult for banks to keep the savers

insulated from the negative interest rates. Savers might also be expected to

pay interest for savings.

Similar currency exchange

rate reactions were seen in Japan after the Bank of Japan announced negative

interest rates in late Jan 2016. The Japanese Yen has risen by almost 6.5% (instead

of the expected fall) against the US Dollars since February 2016. The BOJ, too,

has implemented a tiered system for negative interest rates.

Recently, the rate of

interest on the 10 year German Government bond was hovering around 10 basis

points, very close to the historical low of 7 basis points. The fact that the

bond is a safe government debt makes it an attractive investment option. It

would not be wrong to assume that investors would even subscribe to such high

quality debt even if the interest rate yield was negative.

Summarizing, in some

markets, though negative interest rates have been implemented to control the

valuation of the currency, the results are not in line with the expectations of

the central bank. This makes the situation more interesting and ambiguous, and

more incisive action can be expected from the central banks in the coming months.

Summary

The Repo Rate (The Lending

Rate) and the Reverse Repo Rate (The Deposit Facility Rate) have been long used

as a tool to manage and control the economy by the central banks. Given the

evolving market conditions, rock bottom oil prices, slowing growth in China and

Europe, and significant deflationary pressures across the leading economies,

central banks in these economies are using a previously unheard concept of

negative interest rates.

Countries like Sweden,

Denmark and Switzerland have seen early benefits of this policy. Denmark has

managed to keep the inflation rate within 1% in the last two years. Conducive conditions

have been created in neighboring Sweden to increase the inflation rate near to

the stable levels. Switzerland too is also seeing the economy move from

deflation towards inflation.

On the other hand, in

Europe, the inflation is reducing progressively in the last 4 years, with a

strong risk of Euro Zone slipping into deflation. ECB has increased the

negative interest rates in this background, to prevent the Euro Zone from slipping

into deflation.

Understanding Negative Interest Rates

Reviewed by Vyankatesh

on

Saturday, July 30, 2016

Rating:

Reviewed by Vyankatesh

on

Saturday, July 30, 2016

Rating:

Reviewed by Vyankatesh

on

Saturday, July 30, 2016

Rating:

No comments: